Brian Wesbury Weekly Outlook

26.04.2018 11:48 - First Trust Global Portfolios Limited

Modest Growth in Q1 (23 April 2018)

From mid-2009 through early 2017, the US economy grew at a real average annual rate of 2.2%. Not a recession, but not robust growth either, which is why we called it a Plow Horse Economy.

For the first quarter of 2018, we expect growth of 1.9% at an annualized rate, right in-line with a Plow Horse.

But that doesn’t mean the economy is still a Plow Horse. It isn’t. Growth has picked up, even if last quarter doesn’t show it. Even with a 1.9% growth rate in Q1, real GDP is still up 2.7% from a year ago, and we anticipate an average growth rate of around 3% this year and next year with higher odds of growth exceeding that pace rather than falling short.

Taxes and regulations have been cut and monetary policy remains loose. Look for a significant acceleration in growth in the quarters ahead.

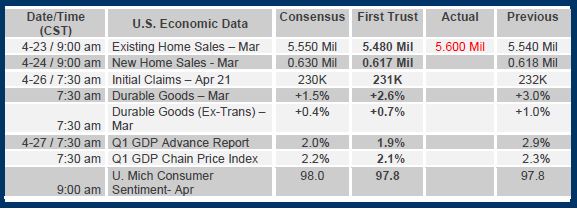

Here’s how we get to 1.9% for Q1. But, keep in mind that we get reports on shipments of capital goods on Thursday as well as early data on trade and inventories, so we could end up tweaking this forecast slightly later this week.

Consumption: Automakers reported car and light truck sales fell at a 12.4% annual rate in Q1, in large part due to a return to trend after the surge in sales late last year following Hurricanes Harvey and Irma. Meanwhile, “real” (inflation-adjusted) retail sales outside the auto sector declined at a 0.8% annual rate. However most consumer spending is on services, and growth in services was moderate. Our models suggest real personal consumption of goods and services, combined, grew at a 1.2% annual rate in Q1, contributing 0.8 points to the real GDP growth rate (1.2 times the consumption share of GDP, which is 69%, equals 0.8).

Business Investment: It looks like another quarter of solid growth, with investment in equipment growing at about a 5% annual rate, and investment in intellectual property growing at a trend rate of 5%, as well. Meanwhile, commercial construction looks unchanged. Combined, it looks like business investment grew at a 4% rate, which should add 0.5 points to real GDP growth. (4.0 times the 13% business investment share of GDP equals 0.5).

Home Building: It looks like residential construction grew at a 5% annual rate in Q1, roughly the same pace as the average over the past five years. This should add 0.2 points to the real GDP growth rate. (5.0 times the home building share of GDP, which is 4%, equals 0.2).

Government: Public construction projects were up in Q1, but military spending declined. Looks like overall real government purchases rose at a 0.6% annual rate in Q1, which would add 0.1 points to the real GDP growth rate. (0.6 times the government purchase share of GDP, which is 17%, equals 0.1).

Trade: At this point, we only have trade data through February. Based on what we’ve seen so far, it looks like net exports should subtract 0.7 points from the real GDP growth rate in Q1.

Inventories: Like with trade, we’re also working with incomplete figures on inventories. But what we do have suggests companies were accumulating inventories more rapidly in the first quarter than at any time in 2017. This should add a full 1.0 point to the real GDP growth rate.

Add it all up, and we get a 1.9% growth rate. More data will come, and we could adjust, but hopes of a blow-out quarter have dimmed in recent months. Nonetheless, the year-over-year growth rate has accelerated, and this slower quarter is just a temporary pause. Corporate sales, incomes, jobs growth, investments, and construction are all accelerating. So will GDP.

Brian S. Wesbury - Chief Economist

Robert Stein, CFA – Deputy Chief Economist