Brian Wesbury Weekly Outlook

06.06.2017 13:27 - First Trust Global Portfolios Limited

Late last week automakers reported selling cars and light trucks at an annual rate of 16.7 million units in May, down 3% from May 2016. If you look at a twelve-month moving average, sales peaked back in April 2016 and have been trending lower, ever since.

Meanwhile, the twelve-month averages for home construction, prices, and sales are still hitting new highs for the current economic expansion.

The Federal Housing Finance Agency (FHFA) index of home prices in March, based on purchases using conforming loans, was up 6.2% from a year ago, exactly the same increase it saw during the year ending March 2016. A broader measure, the national Case-Shiller index, shows prices up 5.8% in the past year versus 5.1% in the year ending March 2016.

In other words, the auto sector is slowing down, while the housing sector keeps plowing along. These sectors are often correlated, but now they are diverging.

In the early 2000s, both auto sales and housing were booming. But both crashed together in the 2008 Panic. Auto and truck sales fell more than 40% from their peak during the Panic of 2008 and bottomed in February 2009 at a 9 million annual rate, the slowest pace of auto sales since the recession in the early 1980s. Relative to the size of the US population, auto sales were the lowest since at least the 1960s.

The situation in the housing market was worse. Housing starts fell roughly 70% during the Panic, to the lowest rate relative to US population since at least the late 1950s.

Although both sectors recovered substantially in the next several years, the nature of the recoveries were very different, which planted the seeds of the recent divergence.

For vehicle sales, the recovery started in late 2009. Then, only four years later, in 2013, auto sales were already back to 15.5 million per year, less than 10% from their previous 2005 high water mark. In the past few years, auto sales kept rising, setting a new record high in 2016.

But those gains were somewhat illusory. They were based on “catch-up purchases” as consumers had let the national fleet of autos and trucks age beyond normal during, and immediately after, the Panic. Demographics suggest the US needs only about 15.5 million new vehicles each year to account for population growth and scrappage. So, now that consumers have made up for lost time, the auto market should (gradually) return to the norm of 15.5 million light vehicle sales per year.

By contrast, the housing market has never fully recovered.

Using similar demographic calculations to those used for autos, we estimate that US builders should be starting about 1.5 million homes per year, including both single-family homes and multi-unit buildings. But while autos hit an upward inflection point in 2009, housing didn’t hit one until 2011.

This leaves plenty of room for further economic upside in this sector. In fact, it’s been so long since builders hit the fundamental target, a temporary overshoot in construction activity (just like in autos) may happen.

The problem is that limits on land use, including some environmental rules, are impeding the housing recovery. In particular, these rules tend to suppress the construction of “affordable” housing as the costs of the rules don’t vary based on the “price point” the builder is focused on and adding a fixed cost has a larger percentage impact on lower-priced homes.

As a result, we may keep seeing more rapid gains in home prices around the country, not because of some sort of “market failure,” or “greed,” but because of the government’s failure to clear a path for the free market to work.

One key issue to watch will be whether the growth in home prices continues to outstrip the growth in rents. That’s been true the past several years, but now home prices have finally come back to fair value on a national average basis.

This is good news. With home prices recovering, builders will become more active and housing will follow the path of vehicle sales…with a lag, helped along by too much government.

This material is issued by First Trust Global Portfolios Limited (“FTGP”) of 8 Angel Court, London, EC2R 7HJ.

FTGP is authorised and regulated by the UK Financial Conduct Authority (register no. 583261).

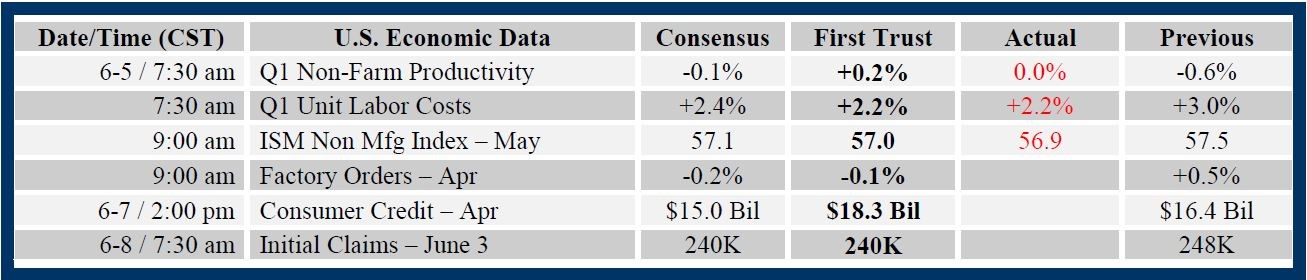

Consensus forecasts come from Bloomberg. This report was prepared by First Trust Advisors L. P., and reflects the current opinion of the authors. It is based upon sources and data believed to be accurate and reliable. Opinions and forward looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security.

Click here to unsubscribe