Brian Wesbury Weekly Outlook

17.05.2018 16:17 - First Trust Global Portfolios Limited

Labor Market Strength (14/05/18)

The US labor market has rarely been stronger.

Recent figures from the Labor Department show US businesses had a total of 6.550 million job openings in March versus 6.585 million people who were unemployed. That’s a gap of only 35,000 workers. By contrast, this gap never fell below 2 million in the previous economic expansion that ended in 2007, and stood at 638,000 in January 2001, at the end of the expansion that started in mid-1991 and ran through early 2001.

Of course, these figures have to be put in context. The measure of unemployed workers doesn’t include “discouraged” workers, for example, nor does it include part-time workers who say they want full-time jobs. And it’s not like all the unemployed have the skill sets needed for the job openings that are available.

Still, the negligible gap between the number of job openings and the number of unemployed who are pursuing work shows that the demand for labor is intense.

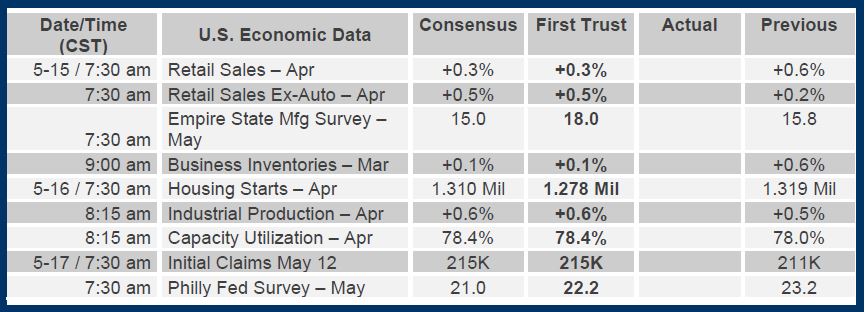

Reports on jobless claims show companies are clinging to their workers. In the past four weeks, the average pace of initial jobless claims has been the lowest since 1969; meanwhile, continuing claims have averaged the lowest since 1973.

And new jobs continue to be created. In the past year, nonfarm payrolls are up an average of 190,000 per month, matching the pace of the year ending in April 2017. As a result of this continued job creation, the jobless rate has dropped to 3.9% in April, the lowest since the peak of the internet boom in 2000.

Assuming a real GDP growth rate of 3.0% this year and next, we think the jobless rate will finish 2018 at 3.7%. That would be the lowest rate since 1969.

Then, in 2019, the jobless rate should drop to 3.2%, the lowest since 1953. Beyond that, continued solid growth could realistically push the jobless rate below 3.0%.

Maybe it’s optimism about the labor market that’s behind President Trump’s recent tick upwards in popularity and the GOP’s better performance in the “generic” ballot, which measures whether potential voters are inclined to support Republicans or Democrats in House races this November. Either way, it doesn’t seem like an environment that favors a tidal wave of change for the Democrats this fall. The odds of the GOP keeping the House are rising, and the GOP looks more likely to gain Senate seats than lose them.

Although some still bemoan slow growth in wages, April average hourly earnings were up a respectable 2.6% in the past year. And that doesn’t include the kinds of one-time bonuses that have become more widespread since the tax cut was enacted in late 2017.

The biggest blemish on the labor market is that the participation rate – the share of adults who are either working or actively looking for work – is still low by the standards of the last forty years. After peaking at 67.3% in early 2000, the participation rate has declined to the current reading of 62.8% in April.

This drop is mainly due to three factors: the aging of the Baby Boom generation into retirement years, overly generous student aid (which has reduced the willingness of young Americans to work), and disability benefits that are too easily available. Hopefully, the coming years will see policymakers find ways to tighten rules on disability while limiting student aid to truly needy students who are taking economically useful coursework.

But even if these changes don’t happen, look for more good news – and an even stronger labor market - in the year ahead.

Brian S. Wesbury - Chief Economist

Robert Stein, CFA – Deputy Chief Economist