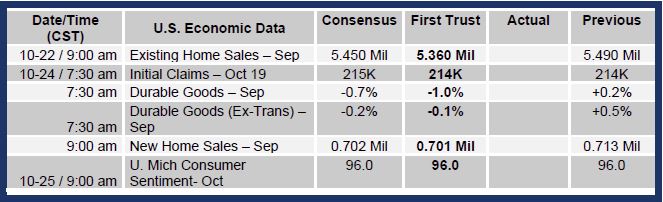

Brian Wesbury Weekly Outlook

22.10.2019 18:55 - First Trust Global Portfolios Limited

More Tepid GDP Growth in Q3

The government doesn’t release its initial estimate on third quarter real GDP for another nine days, but at this point we have enough facts and figures to make an educated guess that it’ll come in at right around a 1.8% annual rate, maybe a little higher, maybe a little lower.

Given that the economy grew at a tepid 2.0% annual rate in Q2, we’re sure you’ll hear plenty of angst about slow growth. But we don’t believe these past quarters represent a permanent shift to slower growth.

Productivity growth (output per hour) has picked up from where it was earlier in the expansion – in our view due to tax cuts and deregulation – and so growth is positioned to re-accelerate. Trade angst has likely caused some downward pressure on production and trade, but hurricane Dorian didn’t help either, and the GM strike took a tenth of a percent or so off growth as well. The strike and storm are temporary effects, and we expect some resolution on trade in the months ahead. Congress could certainly make the trade situation better by passing USMCA (the new NAFTA). And the pressures on both China and the US to sign a first step agreement - or at least call a truce - are high.

In the meantime, monetary policy remains loose for economic purposes, suggesting fears of a recession are overblown. We also like to follow what we call “core GDP,” which is the combined real growth in personal consumption, business investment, and home building. Core GDP looks like it grew at a 2.2% annual rate in the third quarter.

In other words, while the economy may not be booming, the underlying trend remains healthy. Here’s how we get to our 1.8% real growth forecast for Q3:

Consumption: Car and light truck sales grew at a 0.2% annual rate in Q3, while “real” (inflation-adjusted) retail sales outside the auto sector grew at a 3.9% rate. Meanwhile, it looks like consumer spending on services grew at a 1.0% rate. Combined, that would mean real personal consumption (of goods and services combined) grew at a 2.6% annual rate, contributing 1.8 points to the real GDP growth rate (2.6 times the consumption share of GDP, which is 68%, equals 1.8).

Business Investment: It looks like continued investment in equipment and intellectual property was mostly offset by declines in commercial construction. Combined, business investment grew at a roughly 1.0% annual rate in Q3, which would add 0.1 point to real GDP growth. (1.0 times the 14% business investment share of GDP equals 0.1).

Home Building: Residential construction has been flat to negative in each of the past six quarters, and it looks like Q3 was no different, likely coming in at zero change for the quarter. That said, we expect a turnaround in the quarters ahead as home builders are still constructing too few homes given population growth and the scrappage of older homes. In the meantime, a 0.0% pace in Q3 translates into zero net contribution to Q3 real GDP growth. (0.0 times the 4% residential construction share of GDP obviously equals 0.0).

Government: Looks like a relatively small 0.6% increase in real public-sector purchases in Q3, which would add 0.1 point to the real GDP growth rate. (0.6 times the government purchase share of GDP, which is 18%, equals 0.1).

Trade: Net exports’ effect on GDP has been very volatile in the past year, probably because of companies front-running - and then living with - tariffs and (hopefully) temporary trade barriers. Net exports added 0.7 points to the GDP growth rate in Q1, and then subtracted 0.7 points in Q2. We’re expecting a 0.4 point drag in Q3.

Inventories: Inventories are a potential wild-card because we are still waiting on data on what businesses did with their shelves and showrooms in September. We get a report on inventories next Monday, two days before the GDP report arrives, which may change our final forecast. In the meantime, it looks like the pace of inventory accumulation picked back up in Q3, which should add 0.2 points to real GDP growth.

Add it all up, and we get 1.8% annualized real GDP growth. The naysayers will surely use this report to claim victory, but we expect noticeably faster growth in the fourth quarter, led by an improvement in home building and less of a drag from commercial construction.

The bottom line is, nothing in the report will suggest a recession is on the way, or that Treasury yields should remain as low as they are today.

Brian S. Wesbury - Chief Economist

Robert Stein, CFA – Deputy Chief Economist